Investor Transparency is Driving New SEC Rule Changes

Stakeholder Labs joins NIRI in Washington D.C. for an advocacy trip to further investor transparency initiatives

Last month, Stakeholder Labs CEO Matt Joanou joined members of the National Investor Relations Institute (NIRI) on a trip to Washington D.C. to learn about the legislation process and advocate for rule changes that serve in the best interests of investor relations professionals and the public corporations they represent. Given that NIRI often cites investor transparency as the pivotal challenge for IROs, it was quite timely that their visit aligned with the SEC finalizing two rule changes impacting how and when beneficial ownership and short positions are shared with companies and the public. While these rule changes might seem minor, we’ve highlighted in past Roundtable Roundups that digitally disseminated information can swiftly influence markets. This week we dive into the latest rule changes implemented by the SEC and other articles highlighting how investor transparency is becoming a hot-button issue across capital markets and the fintech world.

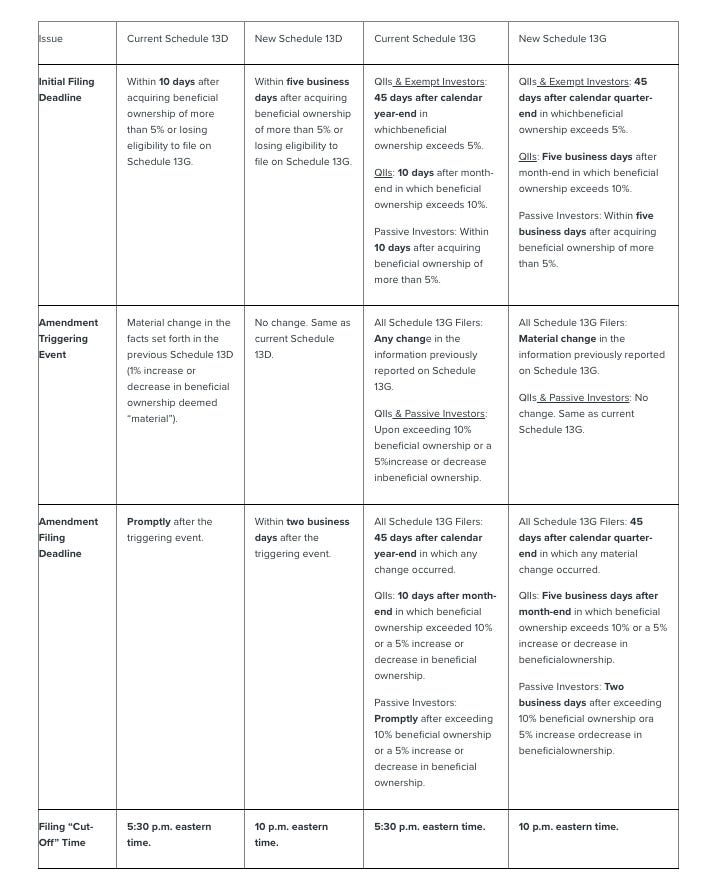

SEC Adopts Amendments to Rules Governing Schedule 13D and Schedule 13G Beneficial Ownership Reporting (Goodwin)

On October 10, 2023, the US Securities and Exchange Commission adopted rule amendments governing beneficial ownership reporting under Sections 13(d) and 13(g) of the Securities Exchange Act of 1934. Exchange Act Sections 13(d) and 13(g), along with Regulation 13D-G, require an investor who beneficially owns more than five percent of a covered class of equity securities to publicly file either a Schedule 13D or a Schedule 13G, as applicable, to report their ownership. An investor with control intent files Schedule 13D, while exempt investors and investors without a control intent, such as qualified institutional investors and passive investors, file Schedule 13G. Until this month’s action, the deadlines for filing the initial Schedule 13D and Schedule 13G had not been updated since 1968 and 1977, respectively. The amendments:

SEC Tightens Rules on Activist Investors Amid Musk-Twitter Investigation (Morningstar)

The SEC has instated new rules demanding activist investors to disclose more swiftly when they've aggressively bought a target company's shares or relevant derivatives.

Investors aiming to take over a company must now disclose within five business days if they've secured 5% or more interest in a company, reduced from the previous 10 calendar days. This adjustment also covers certain derivatives in the 5% calculation.

The push for this amendment arose from the need to shield investors from remaining unaware of significant shares being amassed by activist investors, which can profoundly influence their stock's value.

Elon Musk's acquisition of Twitter last year, where he didn't timely report his takeover intentions after obtaining over 5% of Twitter shares, highlighted the urgency for these rules. Notably, these new regulations won't affect Musk's ongoing case but will guide future transactions.

SEC Chairman Gary Gensler emphasized the importance of reducing "information asymmetry" and ensuring shareholders access vital data more promptly.

Statement on Final Rules Regarding Short Sale Activity (SEC Chair, Gary Gensler)

The SEC is adopting new rules to enhance the transparency of short sale-related data for regulators and the investing public, supporting the initiative for better clarity in market activities.

Stemming from the 2008 financial crisis aftermath, the Dodd-Frank Act called for the SEC to increase short selling transparency. Although some disclosures related to short sale transactions were made by FINRA, Congress felt the need for more in-depth regulation.

Now, investment managers must report their significant short positions in equity securities within two weeks after each month. Specific thresholds have been set, such as $10 million or 2.5% of the total shares outstanding on average during a month.

Following public input, changes were made to the initial proposal. The Commission will disclose aggregated data about large short positions and net aggregated daily activity for each settlement day, aiming to provide a more comprehensive view of market dynamics.

These regulations will offer more detailed short sale data than what's currently provided by entities like FINRA. It also aims to illuminate the actions of institutional investment managers, market makers, and liquidity providers, aiding in understanding market behaviors, especially during turbulent periods.

SEC’s Securities Lending and Short Sale Rules Shed Light on Crucial Markets to Fight Abuses and Market Instability (Better Markets)

The SEC issued final rules mandating securities lenders to disclose key details of their lending transactions, and institutional investment managers to report specific data concerning their short sales.

Stephen Hall, Legal Director and Securities Specialist, emphasized that the opacity in the securities lending market has played a role in past financial instabilities, citing the AIG collapse in 2008 and the trading frenzy around meme stocks in 2021. Hall believes that enhanced transparency could have better equipped regulators and the public to handle these disruptions.

The new rules by the SEC aim to provide clarity about securities lending and short sales. This will assist both lenders and borrowers in ensuring the terms align with market standards, and help the SEC monitor potential risks associated with these activities, like short selling.

While applauding the SEC for enacting these rules, Hall felt that the regulations could be more stringent. He mentioned the SEC's decision to extend certain reporting timeframes for securities lending and increase the short position reporting thresholds for institutional investment managers.

Overall, Hall views these rules as a positive move towards improved market transparency, aiding in the protection of investors and maintaining market integrity.

SEC’s New Hedge Fund Rules Lack an Accountant’s Precision (Bloomberg)

The SEC introduced new rules for hedge funds to report equity short positions, prompting concerns about the undue costs it imposes on investors, as the rules seem to be framed more from a legal perspective than an accounting one.

While the directive to report short positions might appear straightforward, complexities arise for large investment managers who handle myriad funds, accounts, and sub-accounts. Ensuring accurate reporting without double-counting becomes challenging, and penalties for mistakes, even minor ones, can be severe.

The current SEC approach aggregates data by investment manager rather than by the legal entity. This method blurs crucial distinctions the SEC aims to understand, such as distinguishing between those betting against stocks and those hedging or identifying highly levered funds from less-levered ones.

A significant issue with the SEC's method is the lack of clear definitions, particularly around the hedging of short positions. This ambiguity could lead to a majority of positions being categorized as "partially hedged."

A more efficient rule, from an accounting perspective, would be to base the reporting unit on the legal entity and not the investment manager. Only entities with notable net short directional exposure should report, ensuring clarity and ease of reporting.

Other news about investor transparency and corporate control:

Broadridge Financial’s Proxy ‘Monopoly’ Faces Challenge from Start-ups (Financial Times)

Broadridge's Dominance: Broadridge Financial Solutions has long been the leading company in the U.S. for distributing shareholder voting materials, handling tasks like sending out regulatory documents and counting shareholder votes. They claim to manage proxy services for about 80% of shares in the US.

Challengers Are Coming: New companies, such as London-based Proxymity, are trying to break into this market. They believe they can use new technology and the growing interest in shareholder voting among smaller investors to make a dent in Broadridge's dominance. Proxymity, for instance, has received backing from big names like JPMorgan Chase and Deutsche Bank.

Broadridge's Strengths: Despite the competition, Broadridge remains strong. They've developed a mobile app allowing shareholders to vote easily and see all their accounts in one place. Their long history and large client base make it hard for new entrants to dislodge them. Moreover, they argue that their size offers added cybersecurity benefits.

Concerns Over Broadridge's Monopoly: Some are worried about Broadridge's dominant position. Questions arise about the cost implications for shareholders when one company has such control. There are also frustrations over the lack of transparency in Broadridge's fees.

Challenges for New Entrants: While these new companies bring innovative ideas, experts note that breaking into this market is tough. For a start-up to genuinely challenge Broadridge, they'd need a significant company to switch over to their services, which would be a costly and challenging move.

Carl Icahn Bet on the ‘Big Short 2.0.’ Now He Says the Game Was Rigged. (The Wall Street Journal)

The Big Bet: Four years prior, renowned Wall Street investor Carl Icahn made a substantial wager against U.S. shopping malls using credit-default swaps, a form of insurance against bond losses.

Initial Success and Subsequent Decline: Icahn's strategy saw a significant profit of about $900 million in 2020, boosted by the effects of the Covid-19 pandemic. However, by 2022, his positions registered a $742 million loss.

Controversy Surrounding Crossgates Mall: When the mall's debt was up for sale, a notably high bid from Canae Portfolio Advisors ($40M more than any other bid) narrowly avoided triggering a payout. This led to Icahn raising eyebrows at the potential for market manipulation.

Irony of a "Rigged System”: Despite his institutional dominance, Icahn insinuated that the deck might be stacked against him by trading counterparties, touching on sentiments sometimes shared by retail investors about market fairness.

Conclusion

In the evolving landscape of investor relations and financial regulation, the pivotal role of transparency is undeniable. As evidenced by the SEC's recent rules on short position reporting and beneficial ownership, there's a clear push towards shedding more light on the movements of institutional investors. The synchronicity of NIRI’s advocacy trip to Washington D.C. and the SEC's regulatory changes signifies the merging paths of industry initiative and legislative responsiveness. Yet, while the rapid digital dissemination of information serves as a double-edged sword, one cannot ignore the potential repercussions of excessive transparency.

With online communities like r/wallstreetbets closely scrutinizing hedge fund short positions and leveraging these insights for collective actions, the market dynamics are rapidly shifting. Add to this mix the rise of AI tools like ChatGPT and the burgeoning world of copy trading, where individual investors can seamlessly emulate the strategies of seasoned professionals, and the ramifications could be unprecedented. It's precisely this rapidly evolving market context that underscores the inspiration behind Stakeholder Labs' mission.

Recognizing the potential volatility of an overly transparent financial environment, Stakeholder Labs is building technology that aims to foster deeper connections between companies and their shareholders, anchoring investments in genuine corporate value rather than fleeting market sentiments. Amidst the noise of instantaneous data and reactive market behaviors, Roundtable (Stakeholder Labs’ software platform) offers more control and stability by reinforcing long-term shareholder relationships.

Navigating this intricate financial landscape is undeniably challenging. Yet, with innovative technology solutions, there's hope that a balance between transparency, loyalty, and market stability can be achieved, shaping a resilient and inclusive financial future.