Past, Present and Future of Shareholder Rewards

And opportunities to grow brand loyalty and long-termism

The Stakeholder Labs team has been on the road this month with a stop last week in Atlanta for NIRI’s Southeast Regional, Las Vegas earlier this week for Shoptalk and New York City on Thursday for the IR Magazine Awards. We’ve really enjoyed connecting with IR and Marketing leaders and the discussions have accelerated our thinking in a number of areas.

This week’s Roundtable Roundup is focused on the past, present and future of shareholder rewards and how they have been used to increase loyalty between investors and issuers. While dividends and stock buybacks are widely used by companies and are technically considered shareholder rewards, these benefits are accessible to both short-term and long-term shareholders. Stakeholder Labs has been taking a closer look at tenure (or time-based) and consumer rewards as tools for strengthening a company’s retail shareholder community and increasing brand loyalty.

Tenure Shareholder Rewards

Historically, corporate law on both sides of the Atlantic has been rooted in democratic principles and therefore ‘one share, one vote’ has been the pervading system of governance. However, in the 19th century, a French law was passed that allowed companies to grant double votes to shareholders who had held their shares for at least two years. This system became known as "double voting rights" and was widely adopted in France and other European countries including Italy, Spain, Netherlands and Belgium. In 2014, the French Government reinforced tenure voting rights with a new statute, commonly referred to as Loi Florange, where all shares may potentially increase voting rights after a period of at least two years of uninterrupted ownership unless two-thirds of the company’s stockholders vote to opt-out. In other words, in France, tenure voting rights have become the default rule and listed companies that want to adhere to the one share, one vote principle need to opt out of this default loyalty-enhancing mechanism (Caneiro - U of Michigan).

According to the New York Times:

The ostensible purpose of these changes, particularly the new voting rules, is to foster “long-termism” — rewarding French shareholders for holding shares for the long term and committing to the company. It’s a law clearly directed not just at hostile takeovers, but also at shareholder activists and at United States institutional investors, which are increasingly vocal in influencing companies across the globe.

In the US, there has been regulatory resistance to adopting tenure voting rights but many public companies with one share, one vote structures assert that they are unable to shield themselves from short-term shareholder pressure to increase their stock price (Tenure Voting and the U.S. Public Company - Berger, Solomon, Benjamin, 2016). The rapid growth of investment management firms over the last 60 years has transformed US markets resulting in a steep decline in equity holding periods and shareholder loyalty.

According to New York Stock Exchange (“NYSE”) data, between 1960 and 1980, the average holding period of public company stocks ranged from about three to five years. Beginning in the early 1980s, with the rise of the takeover boom, this holding period began to decline. By 1990, the period had fallen to about two years, and by the mid-2000s it was less than a year. The average holding period today for individual stocks across all U.S. markets is about seventeen weeks… The average hedge fund turns over its holdings more than three times a year.

Berger, Solomon and Benjamin identified just twelve US companies in the last 30+ years that have implemented tenure voting plans with limited success, in part, due to the 1980s SEC Rule 19c-4 that prevented companies from adopting dual classes of stock. After the Rule was struck down by a D.C Circuit court in 1990, exchanges implemented similar initiatives but explicitly noted that their voting policies were “more flexible” than Rule 19c-4, and further recognized the need for “additional flexibility in light of the reality that both capital markets and the needs of companies change over time.” While it is difficult to prove a direct correlation today due to the small sample size of companies adopting tenure rewards, it should be noted that an investment in 1980 in an index of the twelve tenure voting companies (including Aflac, Carlisle Companies, J.M. Smucker Company, etc) would be in 2013 worth six times an identical investment in the S&P 500.

Consumer Shareholder Rewards

Consumer shareholder rewards have been utilized by some of the world’s most popular brands with varying levels of success including sunset programs from Disney (personalized stock certificates), McDonald’s (free Big Mac coupon with annual report) and Starbucks (free coffee coupon with annual shareholder report ended in 2019). Other companies have implemented successful consumer programs that increased brand loyalty with measurable results.

Carnival Cruises CCL 0.00%↑ developed one of the most successful US consumer shareholder rewards programs since launching in the 1990s. Shareholders holding a minimum of 100 shares (~$850) are entitled to up to $250 in onboard credit per year. Other cruise operators such as Royal Caribbean and Norwegian have followed suit with similar programs to compete for customer loyalty.

AMC 0.00%↑ Investor Connect launched following a 2021 memestock rally that saw the stock price ~30X in about 6 months between January and June. The stock price has returned to pre-pandemic levels but that hasn't stopped 100,000s of retail investors from joining their shareholder rewards program and qualifying for a free bucket of popcorn.

Berkshire Hathaway shareholders holding just one share of $BRK.B (~$300) qualify for an 8% discount of GEICO auto insurance.

LVMH Shareholders Club offers unique benefits and rewards across the French conglomerate including special access to Hennessy’s centuries old cellars, the crayères at Veuve Clicquot, as well as special offers on a selection of the Group’s wines and spirits and discounted subscriptions to LVMH media publications.

Orix (Japan) and Japan Tobacco Inc. recently scrapped their immensely popular shareholder rewards programs “amid discontent from foreign investors”. Orix’s individual shareholders grew from about 50,000 at the end of March 2014, before the start of the benefit program, to around 820,000 by the end of March ‘22 by offering investors in Japan holding 100 shares (~$1600) access to gifts produced by the leasing firm’s clients around the country. Japan Tobacco provided food products such as frozen udon under its shareholder benefit program, and when the program began in 2004, only about 6% of outstanding shares were owned by individual investors. By the end of 2021, the figure had risen to over 20% or ~$6B increase relative to the market cap.

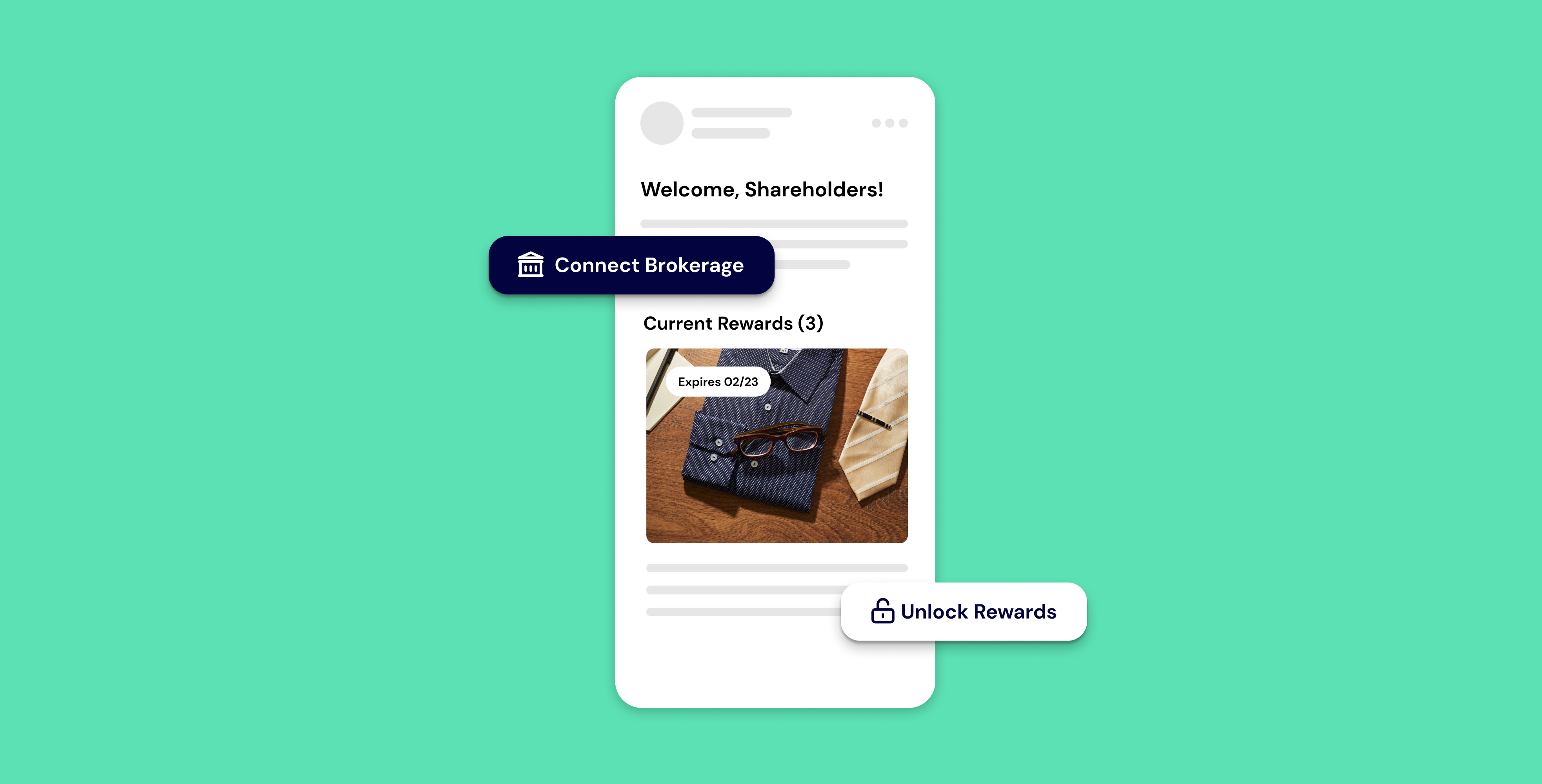

Stakeholder Labs is Unlocking the Potential of Tenure and Consumer Rewards

Shareholder rewards have a long and established corporate history globally and have been used by companies to increase brand loyalty and long-termism. In taking a closer look at the implementation of shareholder rewards, it’s evident that administrative friction and costs associated with tracking the beneficial ownership of a company’s shares is the primary reason why there is not more adoption. If a shareholder wants to verify their stock holdings with Carnival Cruises or LVMH, verification is handled manually via email or mail and this process has to be completed regularly to continue to qualify. In the case of AMC Investor Connect, the company used a self-verification process and literally any person could say they were a shareholder and receive a free bucket of popcorn.

When Berger, Solomon and Benjamin examined the twelve tenure shareholder rewards adopters in the US, over half dropped their programs due to the “impracticality of policing [tenure voting] because of difficulties in determining whether there has been a change of beneficial ownership.” The authors even suggested back in 2016 that blockchain technology, and the ability to automate an immutable ledger of a company’s shareholders, could be a possible solution to the administrative pain points. Becht, Kamisarenka, and Pajuste of the European Corporate Governance Institute (ECGI) concluded that French companies exploring a transition from their default one share, one vote system to Loi Florange-era double voting rules “imposes transaction costs without changing outcomes.”

But what if the administrative overhead and transaction costs could be exponentially reduced with digital shareholder verification?

This is one of our big opportunities at Stakeholder Labs. As we work to establish digital shareholder verification / beneficial ownership as a universal feature for issuers, we’re anticipating a secular shift in the institutional and academic perceptions of tenure and consumer shareholder rewards and we want to be the technology partner powering the most successful programs.

Interested in chatting more about shareholder rewards? Drop us a line!