Year one in review: a closer look at the Universal Proxy Card rule changes

And why retail shareholder may play an increasingly important role in proxy contests

On August 31, 2022, the U.S. Securities and Exchange Commission (SEC) ushered in a significant change in the rules governing boardroom battles at publicly traded companies. The regulation, which was under discussion since 2014 and officially proposed in 2016, addresses the dynamics of proxy contests, situations where a company and a dissenting party - often an activist investor - wrangle over control of the company's board. In the past, each faction would issue separate proxy cards featuring only its own board nominees. This process placed limitations on shareholders who weren't physically present at the annual meeting; they had to select a single card and couldn't mix and match nominees from both the company and the dissident. High-profile proxy battles like Nelson Peltz's $60M+ campaign against Procter & Gamble or Carl Icahn's moves on giants such as Apple, eBay, and Dell show the costs and distractions to management that can result of these corporate skirmishes. According to SEC data between 2017 - 2020, the median costs accrued by companies as a result of an activist proxy contest was $1.7M.

The SEC's new amendment mandates the use of a Universal Proxy Card (UPC), a consolidated list showcasing all candidates nominated by either the company or a shareholder. While both parties involved in a proxy contest can still distribute their proxy cards and related solicitation materials, they must now include candidates from the opposing side on their respective cards. This shift in regulation promises a more democratic and inclusive process, enabling shareholders to voice their preferences more freely and directly influencing the composition of the company's board but it is also poised to make it cheaper for activist investors to engage in a proxy contests.

⛅️ Early Results

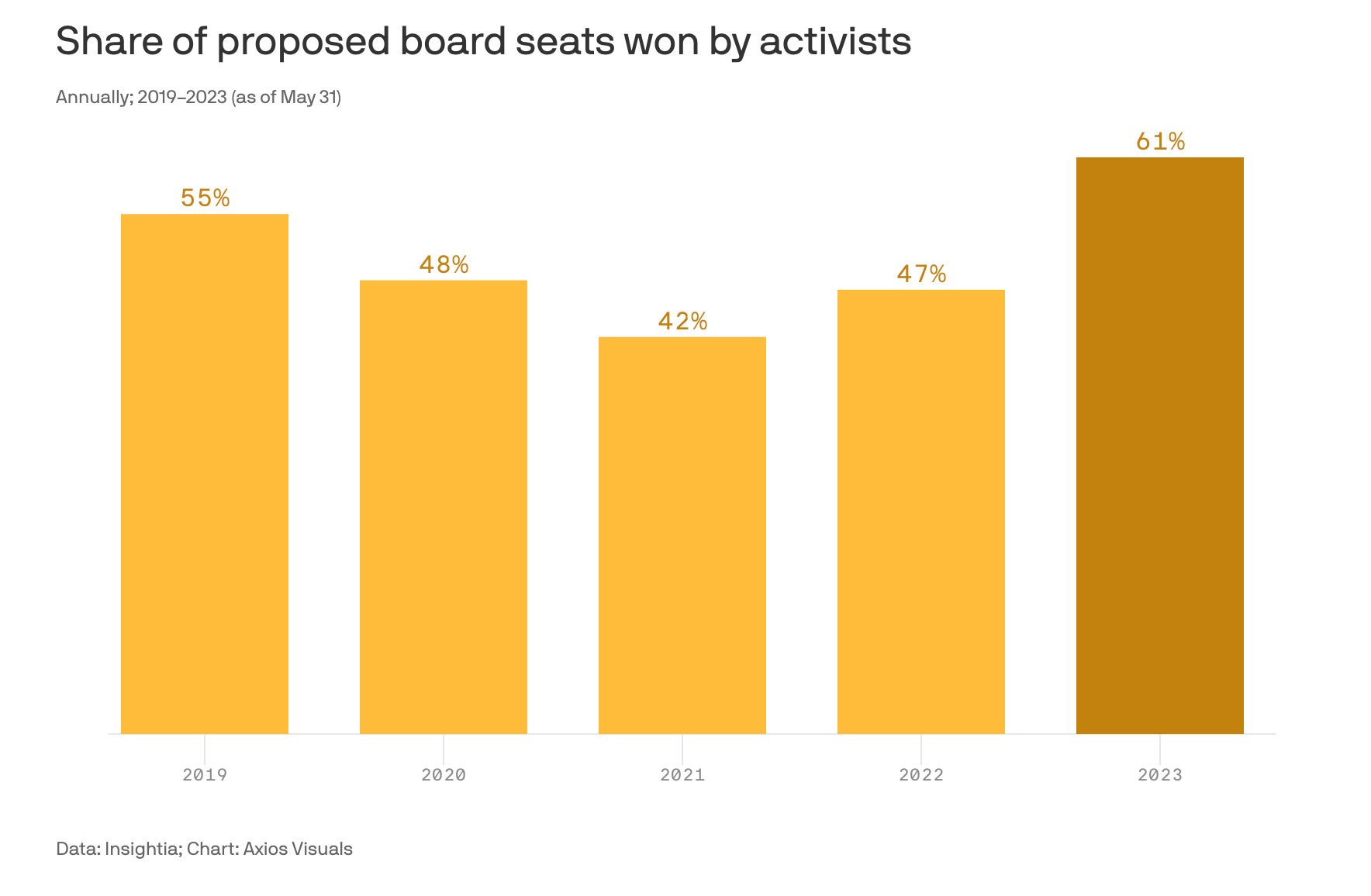

Analysis from the research firm Insightia and Axios show that activist investors were more effective than ever before during the 2023 proxy season. The "win-rate" for activists rose from 47% in 2022 to an impressive 66% this season, a substantial shift that suggests companies might be more inclined to reach settlements before proxy votes to prevent uncertain results. While the number of activist board nominations plunged to 130 in 2023, down from 372 in 2022, this doesn't necessarily indicate a decline in proxy activism. 2023 might just be the quiet before a storm of activism, with many activists potentially held back by the intricacies of advance notice bylaws. These bylaws, often associated with prolonged timelines and exhaustive nominee evaluation processes, may have hindered the full utilization of the new Universal Proxy Card (UPC) rules this year. Interestingly, since the introduction of UPC rules in November 2021, over 556 U.S. companies have updated their advance notice bylaws, specifically disclosure and eligibility criteria or time-related requirements, according to data firm Deal Point Data as of January 28, 2023. These changes suggest a strategic adaptation by corporations to the new UPC landscape, a development we'll be watching closely.

Michael R. Levin, a longtime activist investor and publisher of The Activist Investor newsletter, provided us his initial thoughts on the first proxy season of the UPC era:

It’s a little early in the life of UPC to assess it’s long-term impact. We’ve seen enough situations since the SEC required companies to use it that we can confidently say it has helped activist investors win more Board seats at more companies with somewhat less hassle than before, mostly through amicable if not eager settlement of proxy contests. If the early experience gives us any guidance, we expect even more companies to begin working more closely with activists to not only revamp board membership and corporate governance, but also to consider business turnaround strategies and tactics that these activists would like to see.

🌱 The growing importance of retail shareholders in proxy contests

In the midst of evolving corporate governance norms and ongoing chess games with newly minted bylaws, retail shareholders are poised to play a pivotal role in the future of corporate boardrooms. Historically, the influence of retail shareholders in proxy contests, who own smaller quantities of shares, has often been limited compared to institutional investors. However, the introduction of the UPC, which streamlines the voting process by allowing shareholders to vote for their preferred mix of director candidates from all nominees on a single card, has democratized the process to a greater extent. The traditional two-card system often proved cumbersome and confusing for retail shareholders, thereby limiting their influence. Now, with the simplified one-card system, retail shareholders can more easily participate in board elections, potentially influence the outcomes and more easily support activist nominees. The increased transparency brought by the UPC has the potential to engage retail shareholders more deeply, as it allows for a clearer assessment of each individual director candidate, irrespective of whether they were nominated by management or shareholders.

🧱 Building a ‘margin of safety’ with retail shareholders

UPC changes incentivize companies to engage more directly with their retail shareholders, aiming to build more shareholder loyalty and attract ongoing support for board nominees or other proposals. In the event management is faced with a costly activist campaign, the companies that have established relationships with their retail shareholders and can communicate via inexpensive digital means are going to be at a major strategic and cost savings advantage. This is a significant value creation opportunity for Stakeholder Labs’ digital shareholder verification technology as UPC continues to put pressure on companies to know their shareholders and educate them on company board candidates with personalized messaging, multi-channel content and outreach. This increased dialogue between companies and their retail shareholders could lead to improved corporate governance overall, by ensuring that the interests of all shareholders, not just the large institutional ones, are being considered and addressed.

✍️ Conclusion

As we reflect on the first year of Universal Proxy Cards (UPC), it's clear that this reform will create significant shifts in the landscape of corporate boardroom battles. The adoption of UPC will likely usher in a more democratic and inclusive approach to proxy contests, empowering retail shareholders, and will seemingly benefit activist investors, who have seen an increased win rate this season. However, the significant drop in the number of activist board nominations in 2023 may hint at complexities yet to be fully understood, tied to strategic adaptations such as changes to advance notice bylaws. While the UPC has already begun to reshape interactions between companies, shareholders, and activist investors, its long-term implications remain to be seen, hinting at an evolving frontier in the world of corporate governance. As we move forward, it will be essential for companies to foster stronger relations with retail shareholders and establish a loyal ‘margin of safety’ to deter activist investors. This promises a future of corporate boardrooms that are more responsive and accountable to their diverse range of shareholders.